Smart Ways to Reduce Your Taxes as a Growing Service Business

Stop overpaying! Take back your profit with these easily overlooked or dismissed tax strategies for your business making less than $1M.

When it comes to savvy ways to reduce your tax bill, every stranger on the internet has an idea! Sure, some are great tips and tricks, but not everything you hear about is the right move for your business.

Instead of trying to implement big and broad strategies like incorporating in Delaware or buying a giant SUV, a great place to get started is in the small results that will save you thousands every year. It’s not always flashy, but these strategies will help you keep more money in your pocket when you implement them.

If you don’t have a plan for maximizing your deductions, you’re overpaying.

Good news, it’s fixable!

With the help of year-round tax planning, you can stop making costly mistakes and take control of your profit so you can grow without restraints!

Year-round tax planning isn’t complicated, but it does require taking specific actions. It’s as easy as setting aside 30 minutes monthly to work through this list and save your hard-earned money.

Instead of overpaying, what if you:

Accurately estimated what you owe

Found missing deductions

Proactively avoided penalties

Leveraged the cash you have on hand to grow

Ready to try your hand at year-round tax planning? Start here!

1. Stop Guessing and Estimating! Use Your Numbers to Inform Your Payments.

Most business owners don’t know how much to set aside for taxes. Instead of panicking when you file or wishing you had some extra cash flow to invest in growth, you can take control.

Start with your net income (revenue minus expenses).

Estimate a tax rate based on your location and situation. For many U.S.-based sole proprietors, 25% is a conservative baseline.

Set aside that percentage monthly, not just quarterly.

You can’t manage what you’re not measuring.

When your books are clean and up to date, you can confidently calculate what you owe. No more stressful surprises!

Pro tip: Save this percentage in a separate High-Yield Savings Account. Instead of just sitting around, this allows you to earn interest on it while it’s waiting!

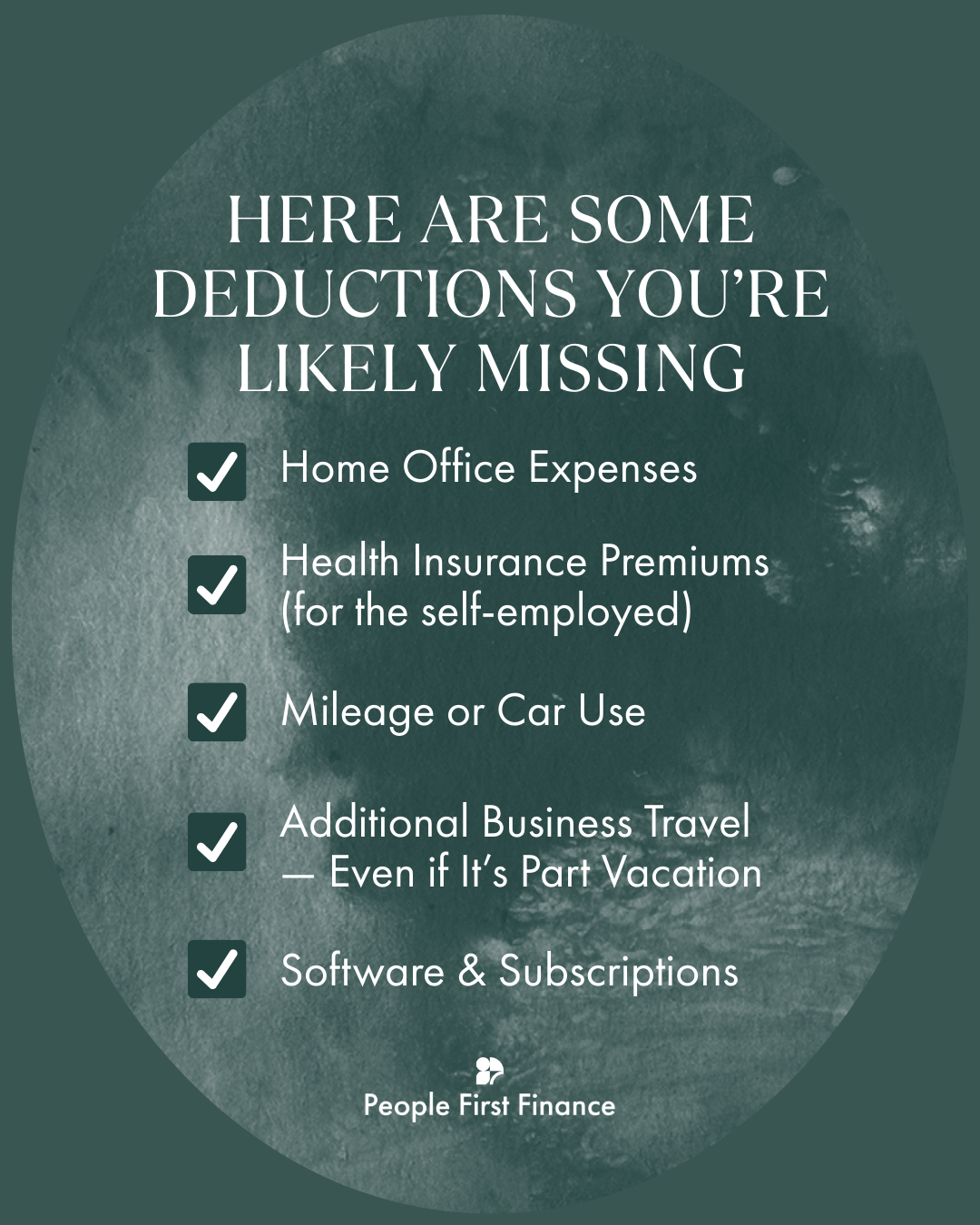

2. Deduct What You’re Entitled To. Here Are Some Deductions You’re Likely Missing!

Tax deductions are your best friend, so track and categorize them properly. Be sure to think outside the box for things such as:

Home Office Expenses

Go one step deeper than pens and paper… You unlock the power of this dedication when you start thinking, “What about the phone and home internet I use to run my business? Or the water, gas, and electric I use during my business hours?”

Most owners think, “It’s not worth tracking,” or they’re afraid of triggering audits, so they skip it altogether. But if done correctly, this is a clean, valuable deduction that adds up.

Strategy: If these are set up under your personal name, you can still deduct a percentage (commonly 50–80%) based on usage. The IRS allows this if it’s “ordinary and necessary” for your business.

Health Insurance Premiums (for the self-employed)

Are you paying out of pocket for your health insurance? Deduct it!

Most business owners assume health insurance isn’t deductible if they don’t have a formal payroll system or believe it only applies to S Corps. Wrong! If you pay the premium monthly, track it for tax time.

Strategy: If you’re a sole proprietor, single-member LLC, or S Corp owner (and not eligible for an employer-sponsored plan), you can deduct your personal health insurance premiums. This includes medical, dental, and long-term care insurance for yourself, your spouse, and dependents.

THIS ONLY APPLIES IF: Your business is profitable. The final dedication can’t exceed your net income. Make it a recurring line item in your monthly bookkeeping so it’s not forgotten later.

Mileage or Car Use

You might not think of your car as a business expense, but every drive to a client meeting, networking event, or office supply store adds up.

Many business owners don’t track mileage in the moment, and once the year’s over, it feels impossible to reconstruct. Others fear they’ll do it “wrong” and invite scrutiny, so they skip it entirely.

Strategy: Mileage has two deduction options, you can opt for:

The standard mileage rate (this is updated often, but currently is $0.70/mile in 2025), or

Actual vehicle expenses (a percentage of gas, insurance, depreciation, repairs)

Most service-based businesses find that mileage is easier. Use a mileage tracking app (like MileIQ, Stride, or QuickBooks mobile), to log your drives in real time. Even 5–10 miles a few times a week adds up to hundreds (sometimes thousands!) of deductible dollars annually.

Additional Business Travel - Even if It’s Part Vacation

Don’t just track your local miles! If you travel out of town primarily for business (think: client meetings, conferences, research), you can deduct travel, lodging, meals, and transportation, even if you also spend a day or two sightseeing!

Strategy: Structure your trip with clear business intent and keep records. Bonus: You can even bring family if their expenses are separated and only your business-related portion is deducted.

Most business owners assume personal travel nullifies the whole deduction. But with proper documentation, this is a legitimate and powerful perk of self-employment. Be sure to confirm with your tax professional what documentation will be necessary before planning to write a trip off.

Software & Subscriptions

The tools you use to run your business can be deduction gold.

Many of these tools are small in cost, and their charges get buried in bank statements. It’s easy to simply forget how many tools you pay for. These small transactions add up!

Strategy: Any software or subscription that serves your business, like QuickBooks, Dubsado, Notion, Calendly, Canva, Loom, Dropbox, or ChatGPT Pro, is deductible. Even website hosting and domain renewals qualify.

The secret is consistency:

Put all subscriptions on a dedicated business card

Review them quarterly (so you’re only paying for what you use)

Make sure they’re categorized correctly in your bookkeeping software

Year-round tax planning isn’t just for big transitions. If you track the little ones, they add up, too! These “small” transactions can work to drastically reduce your taxable income, saving you hundreds every year.

All of these deductions require you to maintain clean and clear books! The IRS loves to triple-check your deductions. If your books are messy, it’s likely to trigger an audit.

3. Pay Your Quarterlies (and Avoid the Penalties)

If you don’t pay estimated taxes throughout the year, the IRS may hit you with penalties—even if you don’t owe much in April.

To stay compliant:

Use your bookkeeping system to project your quarterly profit. Remember: Profit is Income - Expenses. If you start tracking more expenses, you’ll have less profit to account for!

Multiply by your estimated tax rate.

Pay through EFTPS (or your state portal) by:

April 15

June 15

September 15

January 15

Late or missing payments will create an extra cost (though the penalty is small.) However, they tend to weigh heavily on your stress levels and distract you from more important business-related things. If possible, pay them on time to avoid the distraction!

4. Use Your Business Entity Strategically

How your business is structured impacts how much you pay in taxes.

For example:

Sole proprietors pay self-employment tax on all profits.

An S Corporation allows you to pay yourself a “reasonable salary” and take the rest as distributions—potentially reducing your self-employment tax.

But this move only makes sense after a certain income threshold (typically around $80K+ in net profit). You’ll also need to run payroll and file additional forms—so talk to a tax pro before making the switch.

Need help deciding if this is the right move for you? We have this S-Corp Election Resource.

5. Invest in Retirement (and Get the Write-Off)

It’s hard to lower your tax bill and hold onto more of what you earn, but contributing to a retirement account allows you to do just that!

Consider:

SEP IRA

Solo 401(k)

Traditional IRA

These allow you to lower your taxable income while building long-term financial stability. A smart move for your taxes and your future!

Overwhelmed just reading this?

You’re not alone! Many other amazing service business owners put off year-round tax planning because:

It feels overwhelming

They don’t know what’s “normal” or expected

They’ve been burned by bad advice or overpriced pros

Their books aren’t clean enough to make decisions with confidence

And that’s exactly why People First Finance exists.

We don’t just categorize expenses and file taxes. We help you build clarity into your business. We partner with you to understand what’s working, fix cash leaks, and move forward without the guesswork.

Want to learn more about how we do that?